Your Ultimate Guide to Smarter Banking

The financial world is undergoing a dramatic transformation. For decades, the traditional bank, with its fixed hours, physical branches, and familiar tellers, was the only option for managing personal finances. However, the rise of digital-first financial institutions has introduced a new paradigm centered on convenience, value, and accessibility. Many consumers feel trapped by the high fees and low interest rates of their current banks but remain hesitant to make a change due to concerns about security or the lack of a human touch. This uncertainty is often rooted in common financial misconceptions.

This guide is designed to cut through the noise and provide a definitive roadmap to selecting an online checking account that aligns with a modern lifestyle. The analysis and recommendations below are based on a comprehensive review of the modern online banking landscape, equipping a consumer with the knowledge needed to make a truly informed decision. The goal is to ensure a financial institution works harder for a customer, making their financial life simpler, more secure, and more profitable.

Here are the five essential tips for choosing the perfect online checking account:

- Prioritize Low Fees and High-Yield Potential

- Verify Security and FDIC/NCUA Insurance

- Assess Accessibility and ATM Network Coverage

- Evaluate Technology and User-Friendly Features

- Test Customer Support and Problem Resolution

Prioritize Low Fees and High-Yield Potential

A fundamental distinction between online and traditional banks lies in their operational models, and this difference is most immediately felt in the fee structures and interest rates offered to customers. Without the immense overhead costs associated with maintaining a vast network of physical branches and their corresponding staff, online banks are able to operate on a far leaner business model. This efficiency allows them to transfer the savings directly to their customers in the form of superior financial benefits. This is a sustainable business practice, not a promotional gimmick.

For many, the most compelling reason to switch to an online-only institution is the elimination of common, and often costly, bank fees. Traditional banks often charge a monthly maintenance fee, which can range from $10 to $25, to subsidize their physical infrastructure. While these fees can sometimes be waived, it is typically done by requiring a high minimum balance, such as $3,000, in the account. This practice presents a significant financial trade-off for the consumer. Parking a large sum of money in a checking account to avoid a fee carries a hidden cost: lost opportunity. For example, a business that could be earning a 5% return on an investment by using those funds for growth, is effectively losing $150 annually by keeping the money in a low-yield account to avoid a $20 monthly fee.

Online banks have dismantled the misconception that bank account fees are unavoidable. Many digital banks offer checking accounts with no monthly maintenance fees and no minimum balance requirements. Transaction costs follow a similar pattern. Traditional banks may limit free monthly transactions or charge for wire transfers and cash deposits beyond a certain threshold. In contrast, online banks commonly provide unlimited electronic transactions, free bill pay services, and may even reimburse ATM fees charged by other banks.

Another powerful advantage is the potential for earning interest on a checking account balance. Online banks frequently offer annual percentage yields (APYs) that are exponentially higher than those from their traditional counterparts. While traditional banks might pay a nominal 0.01%, online banks can offer rates that are 10 to 20 times higher, or even more. A business with a $50,000 balance in a high-yield online account could earn $250 annually at 0.5% APY, a stark contrast to the $5 they might receive at a traditional bank. This difference of $245 could more than cover a year’s worth of traditional banking fees, fundamentally altering the financial equation for a consumer. The superior interest rates are a direct result of the online-only business model and represent a tangible way a customer’s money can actively work for them.

To illustrate these key differences, a comparison of online and traditional banking models is provided below.

|

Feature |

Online Banks |

Traditional Banks |

|---|---|---|

|

Fees & Costs |

Typically lower, often with no monthly fees or minimum balance requirements. |

Typically higher, with monthly fees and minimum balance requirements to avoid them. |

|

Interest Rates |

Generally higher on both checking and savings accounts. |

Generally lower, sometimes negligible. |

|

ATM Access |

Nationwide fee-free network via partnerships with other banks and ATM networks. |

Extensive proprietary ATM network, but may charge for out-of-network use. |

|

Customer Service |

Primarily digital and phone-based, with some offering 24/7 support. |

In-person service at branches, supplemented by phone and digital channels. |

|

Branch Access |

None. Services are exclusively through websites and mobile apps. |

Extensive network of physical branches. |

|

Cash Deposits |

Can be challenging, often requiring specific partner ATMs or third-party services, which may incur a fee. |

Convenient, with deposits accepted at any branch or branded ATM. |

|

Product Offerings |

May offer a full suite of services, but some can be limited to basic checking and savings. |

Typically offers a wide range of products including mortgages, loans, and investment advice. |

Verify Security and FDIC/NCUA Insurance

A primary misconception that prevents many from embracing online banking is the belief that digital-only institutions are not as secure as brick-and-mortar banks. This is a significant misunderstanding. In reality, reputable online banks are legally required to adhere to the same stringent security and data protection measures as traditional banks. In many cases, their digital-first nature allows them to implement more advanced and robust security technologies.

The foundation of this security is Federal Deposit Insurance Corporation (FDIC) or National Credit Union Administration (NCUA) insurance. It is a basic standard in the industry and a critical factor to verify before opening an account. This insurance protects deposits up to $250,000 per depositor, per FDIC-insured bank, and per ownership category, even in the unlikely event of a bank failure. For a consumer, this provides the peace of mind that their money is safe, a vital consideration for institutions that do not have a physical location to visit if a financial problem arises.

Beyond federal insurance, a robust online bank’s security infrastructure is a multi-layered defense system. It begins with advanced encryption, such as Secure Socket Layer (SSL) and 128-bit encryption, which scrambles private information to prevent unauthorized access and protect data both in transit and in storage. Many online banking apps also offer multi-factor authentication (MFA), which requires at least two types of verification (e.g., a password and a unique code sent to a mobile device) before granting access. Additionally, biometric authentication, which uses unique physical features like a fingerprint or face to verify identity, provides an enhanced level of security for mobile access.

An online bank’s security also extends to proactive, automated fraud monitoring. Over time, the bank’s systems learn a customer’s normal spending habits. If a transaction occurs that seems out of the ordinary, the system can flag it and contact the customer immediately to verify whether the transaction was authorized. This real-time vigilance is a significant advantage over a system that relies on a monthly statement to discover discrepancies.

It is important to recognize that online banking security is a paradigm of shared responsibility between the financial institution and the customer. While the bank provides the technological safeguards, the user must adopt best practices to maintain a secure environment. These include creating strong, unique passwords with at least 12 characters and a combination of letters, numbers, and symbols. It is also crucial to avoid accessing a bank account over unsecured public Wi-Fi networks, which can leave a user’s data vulnerable to interception. Checking bank statements and transaction histories at least once a month is an effective way to spot any suspicious activity early. By taking these steps, a user becomes an active participant in their own financial security, complementing the bank’s advanced technology with their own diligence.

Assess Accessibility and ATM Network Coverage

One of the most frequently cited drawbacks of online-only banks is the absence of a physical branch. This is a valid point for individuals who prefer face-to-face interaction for advice or who require services like cashier’s checks. However, this is not a simple deficiency but rather a strategic choice that is the fundamental driver of the online banking value proposition. The money saved by not maintaining a physical presence is precisely what enables these institutions to offer superior interest rates and a better fee structure. For a customer, the key is to determine if the financial benefits outweigh the convenience of an in-person branch.

While a user cannot walk into a branch for help, modern online banks have developed robust solutions to address the two most common needs that require a physical location: cash withdrawals and cash deposits. Since they do not have their own proprietary ATMs, online banks have overcome this limitation by partnering with large, national ATM networks. These networks, such as Allpoint or MoneyPass, provide access to a vast number of surcharge-free ATMs nationwide, often surpassing the geographic reach of a single traditional bank’s network. Many of the top online banks will also reimburse a customer for any out-of-network ATM fees they may incur, further ensuring that cash access is never a cost.

The greatest challenge for a fully digital institution remains the issue of cash deposits. While depositing a check is effortless with a mobile app’s photo deposit feature, adding physical cash can be tricky, especially for those who handle a lot of cash in their work. Solutions do exist, but they often require extra steps. Some online banks allow cash deposits through specific partner ATM networks. Other workarounds include using a third-party service at a retail store, or even depositing the cash into a conventional bank account first and then electronically transferring it to the online bank. When choosing an online bank, it is vital to inquire about their specific cash deposit policies and fees to ensure the process is manageable and convenient for an individual’s financial habits.

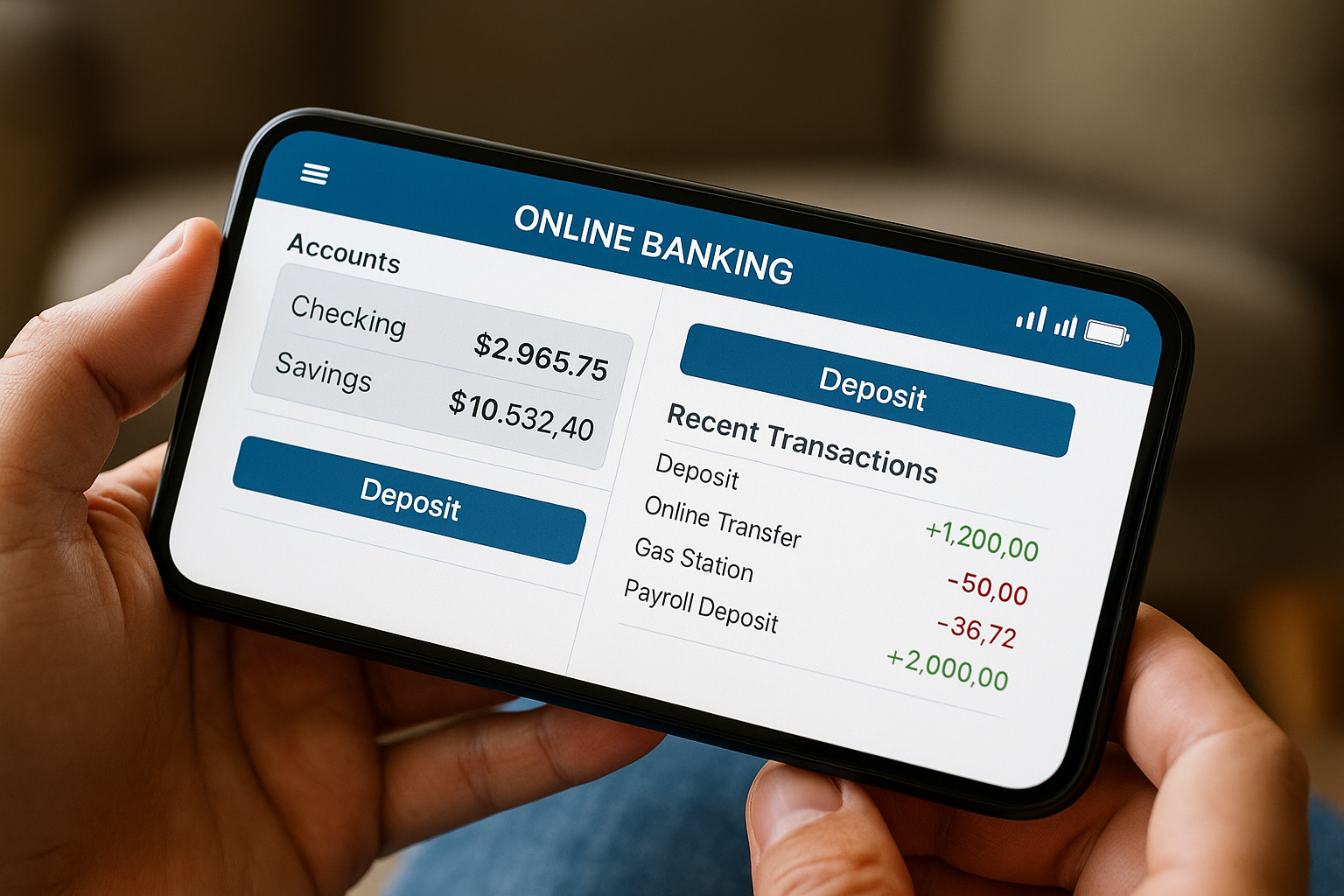

Evaluate Technology and User-Friendly Features

Online banks are often described as “digital-first institutions” because their technology and user experience are central to their services. A checking account with an online bank is not just a place to hold money; it is a dynamic, interactive platform designed to help the user manage and grow their wealth.

The most basic expectation for any modern online bank is a clean, intuitive, and feature-rich mobile app and website. The quality of a bank’s app is a critical factor in the user experience. A clunky or outdated interface can lead to frustration and make it difficult for a customer to stay engaged with their finances. The best online banks provide a seamless digital experience that allows a customer to perform all essential tasks with ease, including:

- 24/7 account access and real-time balance checks.

- Setting up automatic bill payments and scheduling fund transfers.

- Depositing checks using a smartphone’s camera.

- Receiving instant transaction alerts to monitor spending and detect unauthorized activity.

The true value of an online bank’s technology, however, lies in the advanced features that turn a passive account into a proactive financial tool. For instance, many platforms offer holistic money management features that are designed to help customers budget, track spending, and analyze their saving habits. This allows a user to see their financial picture as a single, unified entity instead of fragmented lines on dozens of different statements. Top online banks also incorporate automated savings tools, such as the ability to “round up” debit card purchases to the nearest dollar and transfer the difference to a savings account. This allows a customer to build up their savings without even thinking about it. Some institutions even offer seamless integration with popular accounting software, which is a significant advantage for business customers.

These features collectively represent a fundamental paradigm shift in the relationship between a consumer and their money. While traditional banking is largely reactive—a customer receives a monthly statement and responds to issues—online banking is designed to be proactive and insightful. The choice of an online bank is not just about which one has more features, but which one enables a more engaged, data-driven approach to personal finance.

The table below provides a quick breakdown of how online banks address common fees. This is a powerful demonstration of the financial benefit that a digital-first model can provide.

|

Fee Type |

Typical Traditional Bank Charge |

Typical Online Bank Charge |

|---|---|---|

|

Monthly Maintenance Fee |

$10 – $25, often waived with minimum balance requirements |

None |

|

Minimum Balance Fee |

Fee charged for dipping below a specific minimum daily balance |

None |

|

Overdraft Fee |

$30 – $35 per overdraft |

Often none, or may offer free overdraft protection by linking to a savings account |

|

ATM Fees |

May charge for out-of-network ATMs; can be high if using a non-partner ATM |

None when using partner network ATMs; some reimburse out-of-network fees |

Test Customer Support and Problem Resolution

For all the advantages of modern digital banking, there are moments when human-centric support is indispensable. The ability to resolve complex, sensitive issues—especially those involving fraud or unauthorized transactions—is a critical factor in a customer’s trust and overall satisfaction. While online banks have largely excelled at providing routine, 24/7 digital access for everyday tasks, a significant paradox emerges when a problem requires human intervention.

Online banks provide customer support through various channels, most commonly via phone, online chat, and email. Some institutions even offer support through messenger apps or social media, expanding the avenues for communication and potentially offering faster response times. While this multi-channel system is designed for speed and convenience, it is not without its challenges.

A recent industry study revealed a notable decline in customer satisfaction with online-only direct banks, specifically concerning problem resolution. While overall satisfaction with online banks remains higher than with traditional banks, the ease of resolving issues has dropped sharply. The average time to resolve a problem has increased from 1.9 days to 2.6 days in a single year, and satisfaction with interaction with live phone representatives has also declined. The most significant declines in satisfaction were tied to issues with debit cards, fraud, and unauthorized account activity.

This data reveals a crucial tension within the digital-first model: it is optimized for speed and simplicity in routine, automated transactions, but can struggle with the “off-script,” complex, or emotional issues that require human empathy and a flexible approach. A consumer must be aware of this potential friction point when selecting a bank. The decision should not be based solely on a bank’s ability to handle everyday transactions efficiently, but also on its demonstrated capacity to handle a crisis.

To evaluate a bank’s support, a prospective customer should go beyond simply noting the existence of a phone number. It is recommended to research app reviews and online forums to see how other customers rate the bank’s problem resolution. A customer can even test the support system themselves with a simple question via the online chat or a phone call before opening an account. This proactive approach can help a consumer gauge the bank’s responsiveness and the quality of its support.

Frequently Asked Questions (FAQ)

Q: What information do I need to open an online checking account?

A: To open a checking account online, most financial institutions require a valid, government-issued photo ID, a Social Security card or Taxpayer Identification Number, and proof of a current address, such as a lease or a recent utility bill.

Q: Are online checking accounts safe?

A: Yes, online checking accounts at reputable institutions are as safe as traditional accounts. The primary misconception about their security is unfounded. A key factor to look for is that the bank is FDIC- or NCUA-insured, which protects deposits up to $250,000 per depositor, per account category. Additionally, online banks use advanced security features such as data encryption, multi-factor authentication, and proactive fraud monitoring to protect a customer’s information and money.

Q: How do I deposit cash into an online checking account?

A: Depositing cash can be a challenge with a digital-only bank. While mobile check deposits are effortless, cash deposits typically require a workaround. Many online banks partner with a national ATM network that accepts cash deposits. Other options include using a third-party service at a retail store, or first depositing the cash into a conventional bank account and then transferring the funds electronically to the online account.

Q: How long does it take for deposited funds to become available?

A: There is typically a waiting period for deposited funds to clear. Generally, banks make the first $225 of a deposit available for withdrawal at the start of the next business day after the deposit is made. The remainder is usually available on the second business day, though it is best to check with a specific financial institution for their policies.

Q: What happens if I lose my debit card?

A: Many online banks have features that allow a customer to freeze their debit card instantly through the mobile app if it is misplaced. This prevents new purchases while allowing scheduled payments and transfers to proceed. If the card is unrecoverable, the customer can report it stolen, at which point the card will be deactivated, and a new one will be sent.

Q: Do online banks offer overdraft protection?

A: Yes, many online banks offer overdraft protection and other features to help avoid fees. For example, a customer can often link their checking and savings accounts so that funds are automatically pulled from savings if the checking account balance is insufficient, which can help prevent an overdraft.

Q: Are online banks only for tech-savvy people?

A: The idea that online banks are complicated or only for technologically proficient people is a myth. As digital-first institutions, they are dedicated to making banking as simple and “fuss-free” as possible, with modern, intuitive platforms and mobile apps. These platforms are designed for ease of use and are generally more accessible than a traditional bank’s online services.